Finbro

Leave your reviewFinbro in the Philippines (2025): conditions and loan benefits

This section gives you a high-level view of Finbro before diving into details. Focus on amount, tenor, and repayment channels — these shape your monthly comfort and overall cost. Figures can vary by profile, so always double-check your dashboard before confirming.

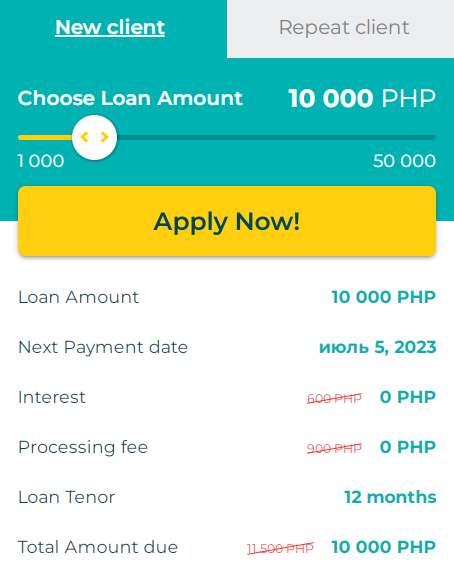

- Loan amount: ₱1,000–₱50,000.

- Tenor: up to 12 months; your final schedule appears in the client dashboard after approval.

- Eligibility: Filipino citizen, 20–70 y/o, stable income; 1 valid ID + selfie.

- Disbursement: to e-wallet (GCash/Maya) or to a bank account; typically fast once the agreement is confirmed.

- Repayment: GCash/Maya (Dragon Loans), 7-Eleven CliQQ (Dragon Loans), MLhuillier/Cebuana/Palawan/SM Bills (via Dragonpay), plus bank transfer from your profile.

- Minimum payment / extension: extend your due date by 7/14/30 days after making a minimum payment; availability depends on your profile.

- Legitimacy: operated by Sofi Lending Inc.

- Typical decision time: ~10 minutes to one working day; updates via SMS/e-mail.

- Good to know: keep payment receipts; real-time posting is fastest via e-wallet or 7-Eleven.

Use the snapshot as a compass: it helps you quickly gauge whether the product fits your needs before you read the specifics.

| Borower Age | 20 — 65 years |

|---|---|

| 1st loan amount | 1,000 — 15,000 PHP |

| 1st loan interest rate | 0% |

| Loan term | 10 — 365 days |

| Repeat loan amount | 1,000 — 25,000 PHP |

| Repeat loan interest rate | 0.2% |

| Money receipt speed | Application processing time can be from 10 minutes to 1 working day during working hours. |

| Types of loans | Fast cash loan, Loan online, Personal loan |

What is Finbro and is it legit?

Finbro is an online microlending platform in the Philippines offering fast cash without branch visits. The service is operated by Sofi Lending Inc. and follows standard KYC and data-protection practices. Expect clear identity checks, defined procedures, and official customer-care channels.

Who can apply (Eligibility & ID)

Before filling the form, make sure you meet the basic requirements. Clean, consistent personal data and a ready ID greatly reduce the chance of delays or rejection. The checklist below outlines what you typically need.

- Age & status: 20–70, Filipino citizen, active mobile number and e-mail.

- Income: stable/regular (employed, self-employed, or other verifiable sources).

- ID (1 piece is enough): SSS, UMID, Passport, Driver’s; Postal ID and PhilID are also accepted.

- Technical needs: a smartphone with a camera for selfie KYC and a stable internet connection.

- Pro tip: names in your form, ID, and e-wallet should match; prepare address details and income evidence if available.

If one criterion is weak, compensate with accuracy and completeness in the rest of your data.

Terms, rates, fees & total cost (TTC)

Choosing well means looking beyond the headline amount and tenor. Rates and fees are shown during application, giving you time to review and decline if needed. Think in TTC terms — what you will actually pay after all costs are included.

- Amount/tenor: ₱1,000–₱50,000 for up to 12 months.

- Rates & fees: disclosed inside the application before you sign — you’ll see the total and the schedule first.

- TTC (Total To pay): principal + interest + applicable fees.

- How to think about it: longer tenors lower the monthly bill but may increase TTC; shorter tenors mean higher monthly payments but lower TTC overall.

- Extras: first-loan promos may be available; always verify them during application.

Write down your total and due dates right away — planning avoids late fees and stress.

How to apply — step by step

The flow is fully online and usually quick. You provide basic details, one valid ID, and a selfie for KYC. After that, you’ll receive a decision and can pick how to receive the funds.

- Choose parameters. Select amount/tenor and tap Apply now.

- Fill the form. Personal data, address, contacts, income source.

- Upload 1 ID + selfie. Use good lighting; ensure all fields on the ID are readable.

- Wait for a decision. From minutes to one working day.

- Review and sign. Check schedule, total cost, and any fees; proceed only if comfortable.

- Receive funds. Choose e-wallet or bank; confirm the credit notification.

Keep your contact details steady until you receive the decision — changing them mid-process can slow verification.

Repayment: channels & mini how-tos

You can repay through popular e-wallets, 7-Eleven, or payment centers — choose what’s fastest and most convenient. Keep receipts and enter references exactly to avoid posting delays. The short guides below help you complete payments error-free.

E-wallet (GCash/Maya):

- Go to Bills → Loan → Dragon Loans.

- Enter the amount, your UM-ID (see dashboard), phone, and e-mail.

- Confirm and save the receipt; postings are typically real-time.

7-Eleven (CliQQ — Dragon Loans):

- Create a bill in CliQQ (app/kiosk), biller Dragon Loans.

- Enter UM-ID and amount; pay at the cashier and keep the receipt.

Payment centers (via Dragonpay):

- MLhuillier, Cebuana, Palawan, SM Bills — select Dragonpay, fill in your name, UM-ID, and amount.

- Posting can take longer than e-wallet/7-Eleven.

Bank transfer:

- Available from your client profile (Bank Transfer). Follow the instructions and keep the proof of payment.

After paying, return to your dashboard to confirm the status. If it hasn’t updated, follow the in-account guidance for support.

Minimum payment & extensions

This option is useful if you can’t pay in full right now. A minimum payment buys time by moving the due date, but your total cost may increase. Treat it as a short-term relief rather than a regular strategy.

- What it does: lets you extend your due date by 7/14/30 days if you can’t pay in full now.

- Trade-off: it doesn’t close the balance; it moves part of it forward and TTC may increase.

- Good use cases: short-term cash gaps, waiting for payroll or expected income.

- Practical tip: enable reminders and calendar alerts; pay early when possible.

If you rely on this repeatedly, consider a smaller amount or shorter tenor next time to reduce strain.

Safety, privacy & avoiding scams

Handle payments only through official channels and follow basic security hygiene. Never share codes or passwords, and always check biller names carefully. The tips below help you minimize risk during the process.

- Use only official billers (Dragon Loans/Dragonpay) and never share OTP/codes.

- Double-check the biller name and save receipts.

- Use your own device and a secure connection; avoid unknown APKs.

- For disputes, use the dashboard and verified support channels.

Where possible, enable two-factor authentication — it’s a small step with big protection benefits.

Pros & cons

Seeing both sides helps you decide with confidence. The pros explain why users pick Finbro; the cons highlight what to plan for in advance. Scan the bullets and map them to your own priorities.

Pros:

- fast decision and fully online process;

- only 1 ID required;

- many repayment options, including GCash/Maya and 7-Eleven;

- minimum-payment/extension option;

- handy dashboard with schedule and reminders.

Cons:

- exact rates/fees appear only during application;

- promos can change;

- late payments can add costs;

- stable income and consistent data are needed.

If the pros align with your needs, go ahead and apply; if the cons are deal-breakers, explore alternatives next.

FAQ

Here are concise answers to the questions users ask most often. Start here if you want quick clarity without reading the entire article. If your question isn’t listed, jump back to the main sections above.

- Is Finbro legit in PH? Yes — operated by Sofi Lending Inc.

- Age requirement? 20–70.

- How many IDs? One (SSS/UMID/Passport/Driver’s/Postal/PhilID) + selfie.

- Is 7-Eleven available? Yes — via CliQQ (Dragon Loans).

- MLhuillier/Cebuana/Palawan/SM Bills? Yes — via Dragonpay.

- Bank transfer? Yes — instructions in your client profile.

- When will I see my rate/fees? During application before confirmation.

- Missed a payment? Check minimum-payment/extension options and pay ASAP to stop costs escalating.

- Can I close early? Usually yes; check your schedule in the dashboard.

- Multiple loans? Depends on risk policy; typically close the current one before applying again.

Remember: your dashboard holds the definitive numbers and dates tailored to your profile.

Contacts

| Official website | finbro.ph |

|---|---|

| Office address | Unit 1405 East Tower Philippine Stock Exchange Center Exchange Road Ortigas,, Pasig City |

| Working time | Mon – Sun: 8am to 5pm |

| Contact number | SMART (969-0471419) GLOBE (917-6200773) |

| info@finbro.ph |

Reviews

{{#items}}-

{{name}}

🗓{{date}}

{{#note}}{{/note}}

{{#reply}}{{/reply}}

{{/items}}